The Memory Supercycle: Why This Time Might Actually Be Different

A boom-and-bust memory cycle line, with the current AI spike marked

A boom-and-bust memory cycle line, with the current AI spike marked

In May 2026, the three companies that make the world's memory each crossed a $1 trillion market cap — Samsung in early May, then Micron and SK Hynix within a day of each other three weeks later. SK Hynix's stock had risen roughly tenfold over the prior twelve months. About a thousand percent. For a company that sells a commodity.

I spend my days financing the machines AI runs on. I buy GPU clusters, build data centers, and turn compute into something you can put on a balance sheet. So I have a professional reason to stare at this chart. The single priciest component inside a modern AI server is not the logic die NVIDIA designs — by most BoM estimates memory is 40-50%+ of an AI server's cost, and on an HBM-heavy training board it rivals the GPU itself. It's the memory stacked next to it. And the businesses that make that memory just had the best year of their forty-year existence. SK Hynix's Q1 2026 revenue nearly tripled year-on-year — ₩52.58 trillion against ₩17.64 trillion, up 198% — and operating profit jumped about 405% to a record ₩37.61 trillion, a 72% operating margin. Samsung's total company operating profit rose about 8.6x year-on-year, as its chip division swung from near-breakeven back to a huge contributor.

The obvious question — the one every investor I talk to is asking — is whether this is real or whether it's the top.

I want to answer it honestly, which means resisting the two easy answers. The bull answer is "AI changes everything, memory is the new oil, buy and hold forever." The bear answer is "it's a commodity, it always crashes, sell." Both are lazy. The truth is more interesting, and more uncomfortable: this run has three structural differences that have never been true at the same time before — and "this time is different" is still the most expensive sentence in finance.

Memory is the most cyclical business in technology, and it's not close

Start with what we are actually dealing with. Memory — DRAM and NAND, the subject of the first part of this series — is the most violently cyclical business in the entire technology stack. Not "somewhat cyclical." The most. The shorthand on trading desks is "up 10x, down 90%," and over four decades that has been roughly accurate.

The reason isn't bad management. It's structural, and four forces compound:

Capacity has a two-to-three-year lead time. A new memory fab costs well over $10 billion and takes years to build, equip, and ramp. The decision to add supply is made years before that supply hits the market — which means it almost always arrives at the wrong moment.

Capex is lumpy. You can't add 5% more fab. You add a fab. Supply comes in giant indivisible steps while demand grows in a smooth curve. The two never line up.

The product is a commodity. A bit of DRAM from Samsung is interchangeable with a bit from Micron. When there's a glut, the only lever is price, and price has no floor — sellers will dump below cost to keep fabs running, because an idle fab loses money faster than a discounted one.

Demand swings hard. A phone cycle, a PC refresh, a crypto boom, an AI buildout — demand spikes, everyone over-orders to secure supply, then the spike fades and the over-ordering reveals itself as a glut.

Put those four together and you get a whip. Tight supply pushes prices up; high prices pull in capex; capex lands two years later into softening demand; glut; prices collapse; capex freezes; the cycle resets. It is the cleanest boom-bust machine in tech.

It helps to see why the magnitude is so violent. Memory fabs have high fixed cost and low marginal cost — once the building, the litho tools, and the cleanroom exist, making one more wafer is cheap. That economics is lovely on the way up and lethal on the way down. On the way up, every extra bit sold at a high price is almost pure margin. On the way down, the rational move for any single player is to keep running the fab even at prices below total cost, because you still cover marginal cost and an idle fab bleeds depreciation for nothing. Everyone reasons that way at once, so nobody cuts output, so the glut clears only when price falls far enough to destroy the weakest balance sheet. That's the mechanism behind "down 90%." It isn't panic. It's arithmetic.

The receipts: this has happened twice in the last decade alone

I don't have to reach for the 1990s to make the point. The cycle ran twice in the last eight years, both times brutally.

The 2017-18 boom: DRAM average selling prices roughly doubled as data-center and smartphone demand outran supply. Samsung's semiconductor division posted record profits; for a stretch its chip business out-earned Intel. Everyone declared the cycle dead, the "super-cycle" had arrived, memory was now a structural-growth story. Then 2019 happened — DRAM prices fell roughly 40% in a single year as the glut showed up. The super-cycle narrative evaporated.

Then it ran again. The 2021 pandemic-driven boom — every device needed more memory, supply was tight, prices climbed. And the 2022-23 bust was one of the worst in the industry's history. Micron and SK Hynix swung from record profits to multi-billion-dollar quarterly losses. Samsung's chip division saw operating profit collapse — it barely broke even in 2023, a near-total wipeout of the most profitable business inside the most profitable hardware company on earth. Fabs ran below cost. Everyone cut capex and prayed.

That bust ended barely two years ago. The same people now calling this an AI super-cycle were, in early 2023, writing memory's obituary. Keep that in mind.

Notice the rhythm. Each peak arrives wearing the same costume — a new structural demand story that proves the cycle is over. In 2018 it was "data center plus mobile, this is structural." In 2021 it was "the whole world went remote, every device needs more memory, this is structural." Both were partly true, and both peaks were followed by sharp 40-50%+ price collapses inside eighteen months. The narrative being plausible has never been a defense. The 2018 and 2021 stories were also plausible. That's exactly why they were dangerous.

There's a second-order point in those two cycles worth sitting with. The gap between peaks shrank — 2018 to 2021 is three years; the recovery out of 2023 into this run took barely two. As the industry consolidated and demand drivers stacked up, the cycles got shorter and the swings, if anything, got faster. That's not evidence the cycle is dying. It's evidence the cycle got more responsive — which is precisely what you'd expect when three coordinated players can turn capex on and off faster than twenty fragmented ones ever could. A faster cycle is still a cycle, and a faster cycle can turn faster than you can react.

The survivors got fewer, which is half the story

There's a second pattern hiding inside the cycle history, and it matters more than the price swings: every bust kills players.

In the 1990s there were dozens of DRAM makers. Each crash thinned the herd. Germany's Qimonda went bankrupt in 2009 after the financial-crisis price collapse. Japan's Elpida — itself a merger of survivors — went bankrupt and was absorbed by Micron in 2013. By the time the dust settled, three companies controlled the entire DRAM market: Samsung, SK Hynix, and Micron, together more than 95% of supply. NAND is slightly less concentrated but tells the same story. The cycle didn't just move prices. It manufactured an oligopoly.

That oligopoly is the hinge of the entire bull case. Hold onto it.

It's worth being precise about why consolidation changes the cycle's character rather than its existence. A market with twenty makers is a coordination nightmare: someone, somewhere, is always desperate enough to cut price for cash flow, and that single defector forces everyone down. A market with three makers is a repeated game between players who will face each other again next cycle, who each have enough share that flooding the market mostly cannibalizes their own margin, and who all watched the 2023 bloodbath from the inside. Game theory says cooperation is far easier to sustain with few players and long memories. It doesn't abolish the prisoner's dilemma — it just makes the cooperative equilibrium more reachable. That's a real change in the depth and duration of the downturn. It is not a change in whether downturns happen.

Three of the five bull arguments were simply not true a cycle ago

Here is the bull case, laid out as five structural claims. I'm going to state each one as strongly as it deserves, because some of them are genuinely new. Then I'm going to come back and weigh the other side.

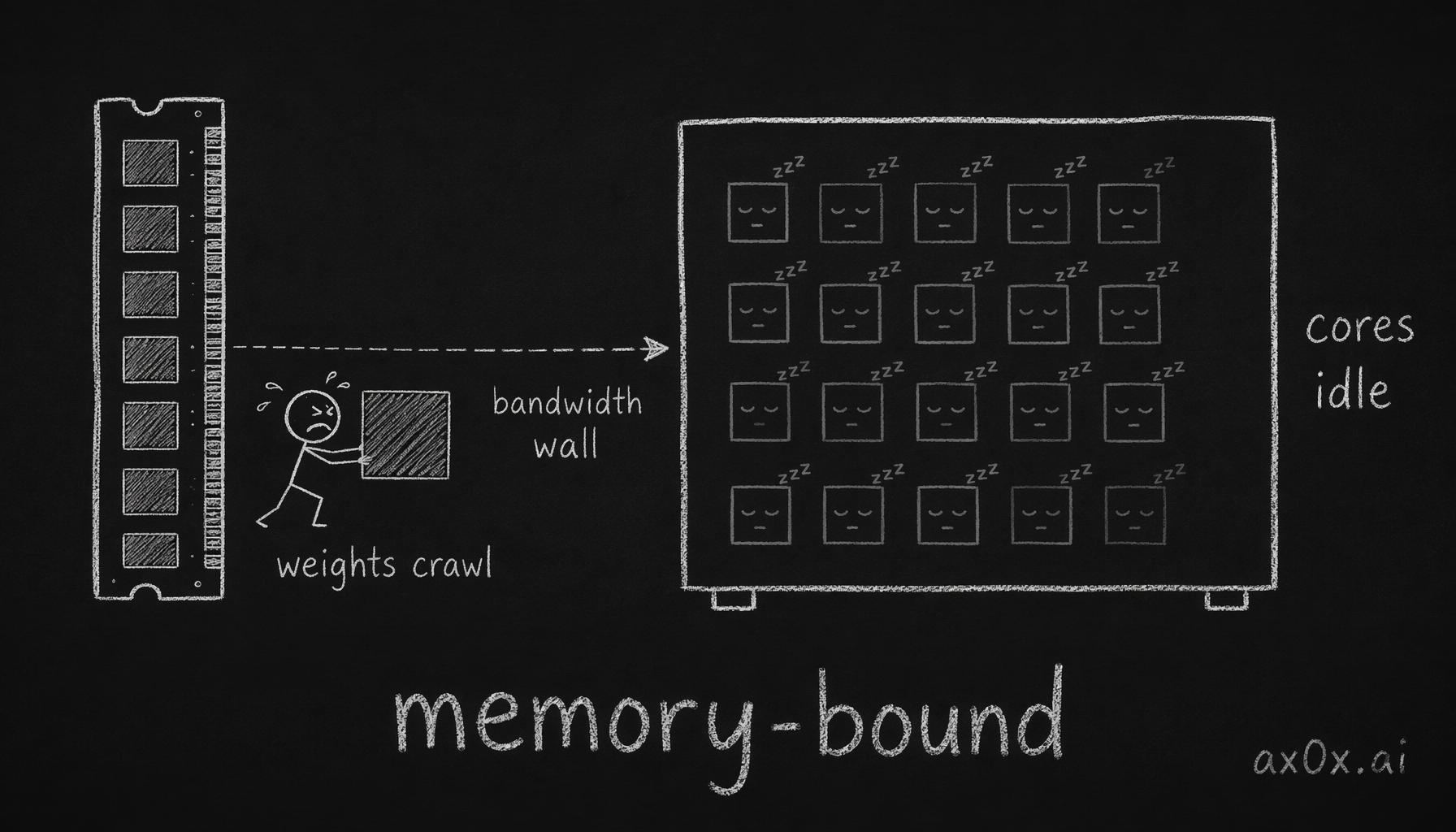

One: the demand is structural, not a restock. Past booms were inventory cycles — PCs, phones, a crypto blip — demand that spikes and then stops. AI demand has a different shape. It isn't one product refresh; it's HBM for training, high-capacity server DRAM for inference, and enterprise NAND for data lakes, all rising at once and reinforcing each other. Every new model generation needs more memory per chip, and there are more chips. And the inference side has its own appetite that didn't exist at the last peak: long-context models and agent workloads turn memory capacity and bandwidth into the binding constraint on how many users you can serve per box — the memory wall I opened the series with isn't an abstraction, it's a line item in every hyperscaler's capacity plan. This is the same argument I made about compute being the root of all intelligence: the demand driver isn't a gadget cycle that exhausts itself, it's the buildout of a new computing substrate. That doesn't make it un-cyclical. It makes the trend line underneath the cycle steeper.

During inference the GPU compute cores sit mostly idle; memory bandwidth and capacity become the binding constraint on how many users one box can serve

During inference the GPU compute cores sit mostly idle; memory bandwidth and capacity become the binding constraint on how many users one box can serve

Two: supply discipline from a three-player oligopoly. In the old days, a glut triggered a price war — someone always broke ranks to grab share. Three rational players who all remember 2023 behave differently. Through this run, all three have prioritized average selling price and profit over volume share, and held capex relatively tight rather than racing to flood the market. The clearest tell is how they handled the 2023 trough: instead of fighting for share, they coordinated — implicitly, through public guidance, not a smoke-filled room — on output cuts to drain the glut, and they let HBM, not commodity bit growth, lead the recovery. Discipline isn't a law of nature; it's a choice, and choices can break. But a three-way standoff is structurally more stable than a twelve-way one — fewer players, repeated games, and every CEO carrying the scar tissue of the last war. This is the dividend the cycle paid by killing everyone else.

Three: long-term agreements that lock volume, not price. This is the genuinely new commercial structure, and it's underrated. The hyperscalers buying HBM aren't placing spot orders; they're signing multi-year supply agreements — and crucially, many lock volume but not price (锁量不锁价 is how I think of it). Some customers are prepaying or effectively underwriting fab capex to guarantee allocation. That changes the risk. The classic glut comes from speculative capacity built on hope; capacity built against a signed volume commitment is a different animal. It doesn't kill the cycle, but it dampens the worst failure mode — building a fab for demand that never shows.

Four: HBM physically crowds out commodity DRAM. This is my favorite structural argument because it's just geometry. HBM uses roughly three times the wafer area per bit of standard DRAM — you're stacking dies, adding TSVs, sacrificing yield, as I walked through in how HBM actually works. So every wafer a fab redirects to HBM is a wafer not making commodity DRAM. HBM content per flagship GPU has roughly doubled about every two years — 80GB on the H100 in 2022, 288GB on the B300 in 2025. As HBM eats wafer capacity, the commodity DRAM that goes into your laptop and phone gets structurally tighter. You saw a preview in 2025: as the Big Three signaled they'd wind down legacy DDR4 and reallocate fabs toward DDR5 and HBM — and with China's CXMT shifting its output mix — buyers panicked into last-time-buy orders and DDR4 prices spiked. The HBM boom isn't isolated to HBM; it tightens the whole stack.

Five: structurally higher margins. HBM is not a commodity in the way DDR5 modules are. It's co-engineered with the customer, capacity-constrained at the packaging step (TSMC's CoWoS gates supply as much as the DRAM does), and sold at materially higher gross margin than commodity DRAM. The product mix is shifting toward the high-margin end. The HBM market was roughly $35 billion in 2025, and is projected toward $100 billion by 2028 at around 40% CAGR (Micron IR), with 2027 estimates spanning $68-90 billion across TrendForce, Yole, and JPMorgan — and it's the slice of memory revenue that doesn't behave like a commodity. HBM already consumes 20%+ of DRAM wafer capacity and rising, with SK Hynix holding 50%+ of that market. Even at the same total revenue, the earnings quality is better than in any prior peak, because a larger share of it comes from product the customer can't simply buy cheaper from someone else next quarter.

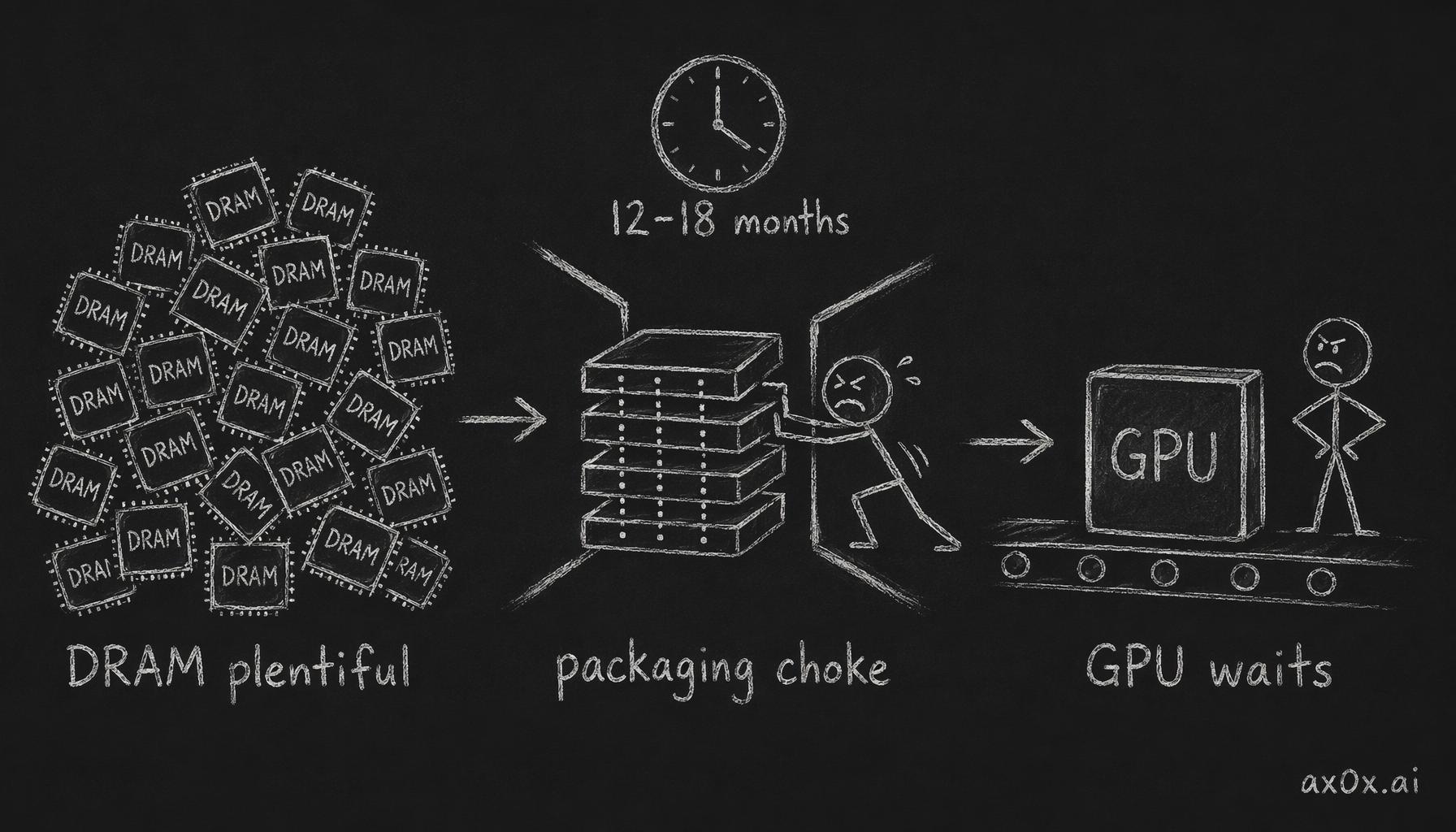

HBM supply is gated not by DRAM dies but by the packaging step — a 12 to 18 month expansion cycle so slow that GPUs arrive before their HBM does

HBM supply is gated not by DRAM dies but by the packaging step — a 12 to 18 month expansion cycle so slow that GPUs arrive before their HBM does

Read those five together and the bull case is genuinely strong. Three of them — the oligopoly discipline, the volume LTAs, and the HBM wafer crowd-out — were simply not true in 2017 or 2021. That's why I won't dismiss this as "just another peak." Something real has changed.

Now the part where I refuse to cheerlead

I don't get to write all of that and stop. The first rule of not losing money is to argue against your own position as hard as you argued for it. Here's the bear case, with full weight.

The run is enormous and the easy money is gone. A stock up tenfold in a year is not pricing in a normal future. It's pricing in the bull case — all five pillars holding, indefinitely. When the consensus has fully adopted "this time is different," most of the return has already been paid out to whoever bought during the 2023 obituary. Being right about the industry and right about the entry price are two different skills.

Double-ordering is invisible until it isn't. The single most dangerous dynamic in a memory shortage is double-ordering: terrified of allocation, customers order from everyone and order more than they need. That demand looks structural right up until it evaporates. We have no clean way to see, from the outside, how much of today's order book is genuine consumption versus inventory hoarding. Every prior glut was preceded by demand that "looked structural." And the LTA structure I just praised cuts both ways here — a multi-year volume commitment is reassuring when it reflects real consumption, but if some fraction of those commitments were signed out of allocation panic, they're tomorrow's phantom demand wearing a contract. A signed order is only as real as the buyer's ability and willingness to take delivery when their own end-demand softens.

Capacity is coming. Discipline holds — until the profits are too good to ignore. All three are expanding HBM capacity, HBM4 is ramping in 2026, and new fabs decided on during this boom will land in 2027-28. And there's a wildcard outside the oligopoly: China. CXMT is sampling HBM (reportedly to Huawei) with realistic volume in the 2027-28 window, and Xiaomi is reported to have taken a stake in CXMT — the "to lock supply" reading is my interpretation, not a stated fact, but the direction is clear enough. A subsidized fourth entrant motivated by national self-sufficiency rather than quarterly margin is exactly the kind of player that doesn't respect a price-discipline equilibrium. Even if CXMT's HBM is a generation behind, it can absorb the commodity DRAM end and free the Big Three's wafers — or, less happily for the bulls, it can simply add bits to a market that didn't ask for them. The oligopoly is being tested from inside and from outside, and the supply that's being committed today arrives precisely when the demand picture is least certain. That two-to-three-year lead time cuts both ways: it's why supply lags a boom, and it's why supply floods a top.

AI capex itself could digest. The whole demand thesis rests on hyperscaler capex continuing to compound. If model-efficiency gains, an inference-cost reckoning, or simple ROI scrutiny slows that buildout even briefly, the memory order book softens immediately — and a softening order book in a commodity market doesn't glide, it gaps. I believe in the compute thesis, but believing in the long arc is not the same as believing every quarter goes up.

The "solutions" to the wall are also threats to the mix. The same demand that makes HBM scarce is funding the next architectures — HBF, CXL pooling, KV-cache offload tiers that spill cold data from HBM down to NAND. NVIDIA's CMX, for instance, is a DPU-managed tier that pushes cold KV-cache out of HBM onto NAND; SanDisk's HBF claims 8-16x the capacity of HBM with comparable system cost and samples in 2H2026. None of these replace HBM — they extend it, the subject of the final part of this series. But to a memory bull, they're a reminder that every supply constraint invites an end-run, and end-runs change which products carry the margin. The mix that's so profitable today is not guaranteed to be the mix two cycles out.

Mean reversion has never lost. This is the one that should keep you honest. For forty years, every single time the industry declared the cycle structurally broken, the cycle came back and collected. 2018 said super-cycle; 2019 crashed. The base rate on "this time is different" in memory is brutal, and no amount of beautiful structural argument changes a base rate — it only changes your estimate of the odds at the margin.

What it looks like from the financing seat

Let me say plainly why I care, beyond intellectual interest. When my firm underwrites a GPU cluster, we are not just betting on NVIDIA's logic die — we're implicitly long every component whose price feeds into the cost and the residual value of that machine, and memory is the largest of those after the GPU itself. A memory super-cycle that's real raises the replacement cost of every cluster on our books and tightens the supply of the next ones. A memory cycle that's about to roll over does the opposite. So I'm forced to hold a view, and I'm forced to hold it without the luxury of cheerleading, because the downside of being wrong shows up directly on a balance sheet I'm responsible for.

That seat teaches one discipline above all: separate the asset from the price of the asset. Compute is the root of all intelligence — I've staked my career on that — and the memory stacked next to it is genuinely scarce and genuinely strategic. None of that tells you what it's worth after a tenfold run. The infrastructure thesis and the trade are different objects, and confusing them is how people who are right about the future still lose money.

A calibrated judgment, not a verdict

So which is it. Here's where I actually land, and it's deliberately not a clean answer.

I wrote once about the lobster fever — how lobster went from prison food to luxury in fifty years without the lobster changing, only the story around it changing. The discipline that essay demands is to separate the narrative from the reality, and ask: strip the story away, is the thing actually worth more?

Run memory through that filter and you get an unusual result. Unlike the AI application layer — where I think a lot of the value really is just narrative — the memory story has real reality underneath it. The demand is structural. The discipline is new. The HBM crowd-out is physics, not vibes. Three of the five pillars are things that were genuinely not true a cycle ago. This is not a pure lobster.

But it is also not the end of cyclicality. Structurally higher trend growth riding on top of a cycle is still a cycle. The trend line got steeper; the oscillation around it did not disappear. The honest position is that the amplitude of the next downturn may be smaller and the floor higher than in 2023 — and that the run has already priced a great deal of that in.

The trap, both ways, is collapsing two separate questions into one. Question one: is the industry structurally better than it was a cycle ago? I think the answer is clearly yes — three real changes, the kind that move the floor. Question two: at a tenfold run in twelve months, is the price still attractive? That's a completely different question, and a strong yes on the first does nothing to answer it. The most expensive error in this whole domain is letting a correct industry thesis launder a careless entry. The industry being durably better is the bull's best card. It is not the same card as the stock being cheap.

The cheap mistake here is symmetry-blindness — either "commodity, will crash, ignore it" or "AI changes everything, hold forever." Both refuse to do the actual work, which is to weigh a genuinely-changed structure against a base rate that has never lost. My read: the demand is real, the discipline is new, the geometry is on the bulls' side — and I would still never forget that "this time is different" is the most expensive sentence anyone has ever said with a straight face about this industry.

The cycle isn't dead. It just learned to climb while it breathes. Where the wall goes from here — and what gets built to climb over it — is the last part of this series.