From Technique to the Way — Your Agent Is a Mirror

Chapter 10 of 10 in the AI-Native Investor curriculum.

Nine chapters taught you a set of techniques. How to read a financial statement as three lenses instead of a thousand lines. How to treat a DCF as a story with numbers attached. How to write a thesis that your future self can argue with. How to command a fleet of agents that research faster than any individual could, and how to catch them when they are wrong.

Techniques are necessary. They are not sufficient.

There is a difference between knowing how to use a tool and knowing when to put it down. Between having a framework and having the judgment to override it. Between being able to analyze a company and being able to sit with the answer — even when the answer is "do nothing."

This chapter is about the space between technique and judgment. The Japanese martial arts tradition calls it the transition from jutsu (technique) to do (the way). In investing, it is the difference between someone who can run an analysis and someone who can make a decision they will not regret in ten years.

Table of contents

- What you built — and what you didn't

- The mirror principle

- What compounds

- The right to do nothing

- The twenty-five-year view

- Workshop: a letter without an agent

1. What you built — and what you didn't

Over nine chapters, you assembled a specific set of capabilities.

You can decompose a stock's historical return into its three sources and ask which one you are betting on going forward. You can read a 10-K through three lenses and identify the patterns that matter — margin structure, debt trajectory, cash flow quality — without getting lost in footnotes. You can build a valuation that makes its narrative assumptions explicit, and you know which assumption the number is most sensitive to. You understand that risk is not volatility but the probability of a loss you cannot afford. You have written at least one thesis with kill criteria and survived having it attacked. You have designed a multi-agent workflow, executed it, and documented where it broke.

That is a real set of skills. Most retail investors do not have them. Many professional analysts have some of them but not all.

Here is what you did not build: experience.

Frameworks are scaffolding. They organize your thinking and prevent certain categories of mistakes. But they do not substitute for the pattern recognition that comes from making decisions with real money, watching those decisions play out over years, being wrong in ways you did not anticipate, and updating your mental models based on what actually happened rather than what you thought would happen.

Charlie Munger spent sixty years building what he called a "latticework of mental models." The lattice was not a curriculum he completed. It was the residue of thousands of decisions, each one teaching him something that no amount of reading could have taught. The curriculum you just finished is the first layer of scaffolding. The lattice takes a lifetime.

This is not false modesty. It is the honest assessment of what a curriculum can and cannot do. What it can do: give you a starting framework, teach you to use powerful tools, show you the shape of the questions that matter. What it cannot do: give you conviction under drawdown, teach you your own psychological weak points, or replace the slow accumulation of judgment that comes from years of paying attention.

What Bloomberg still has

There is a version of this curriculum's thesis that overpromises. It goes: "Agents democratized investing, so now anyone can compete with institutions." That is half true and half dangerous.

Agents closed the analytical tooling gap on public data. That is real. But institutions still have advantages that agents cannot replicate:

Proprietary data feeds — alternative data from satellite imagery, credit card transactions, supply chain tracking, web scraping at industrial scale. These cost millions per year and are not available through public APIs.

Speed — institutional trading systems operate on milliseconds. Bloomberg's news feeds are faster than public media by minutes, and in markets, minutes translate to money. No amount of agent prompting compensates for this.

Relationships — a portfolio manager who has covered a sector for fifteen years has relationships with management teams, suppliers, and industry contacts that produce information no filing contains. An agent cannot have a dinner conversation with a CFO.

Accumulated sector expertise — an analyst who has followed semiconductors through three full cycles has pattern recognition that no model trained on public text can replicate. They have seen what a demand downturn looks like before the numbers confirm it.

The honest framing: agent-assisted investing is an extraordinary training ground. It lets you practice the full cycle — research, valuation, thesis, risk assessment, decision — at minimal cost, with feedback loops that used to be available only inside a fund. It does not make you an institutional investor. It makes you a better-informed individual investor who understands what they are doing and why. That is valuable. Pretending it is more than that is not.

2. The mirror principle

There is a pattern you may have noticed across the workshops.

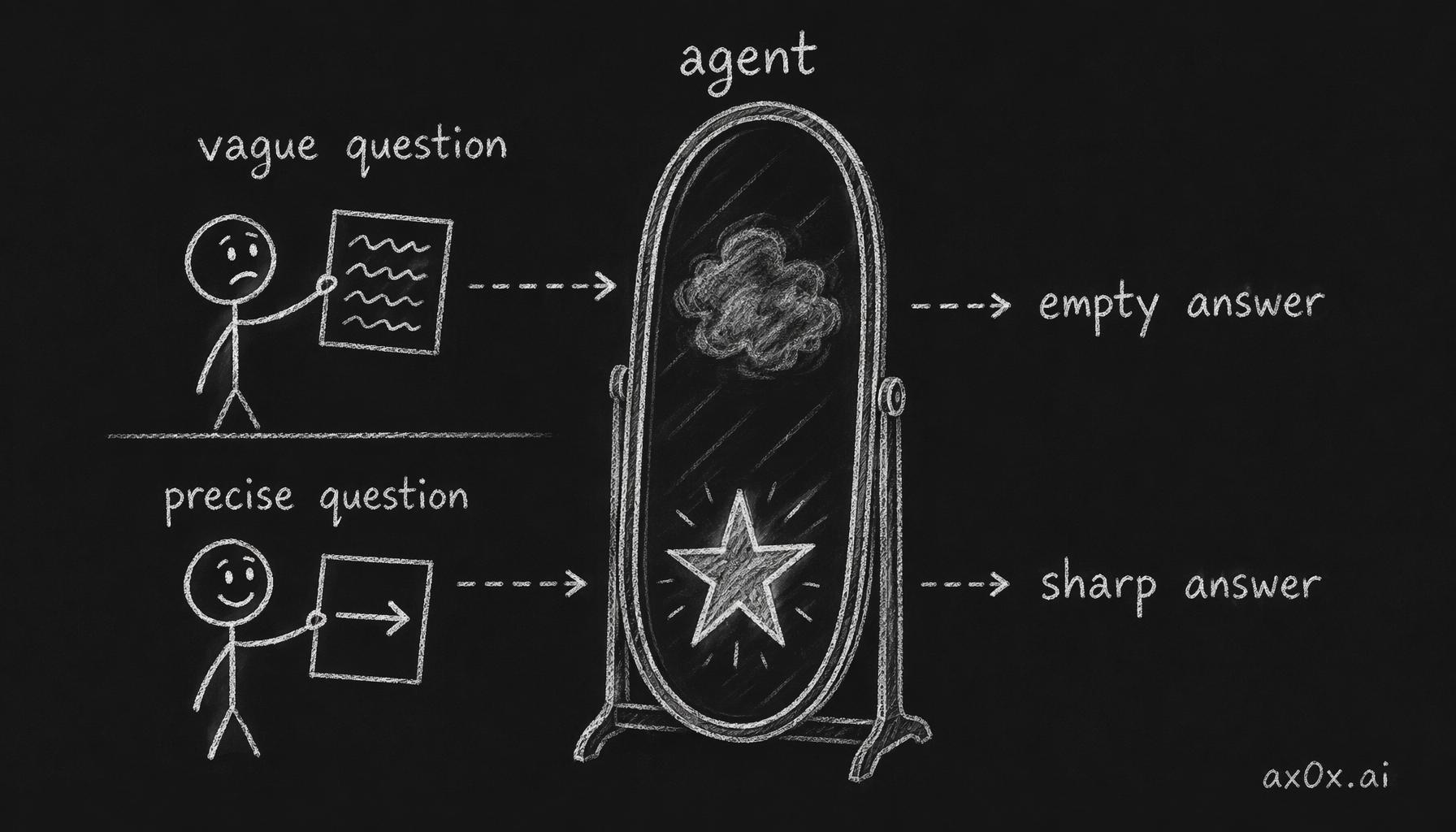

When you asked your agent a vague question — "Is NVDA a good investment?" — you got a vague answer. A balanced, hedged, consensus-flavored summary that told you nothing you could not have found in a two-minute web search. The output was not wrong. It was empty. It had the shape of analysis without the substance.

When you asked a specific question — "NVDA's data center revenue grew 122% last year, driven primarily by hyperscaler orders. What happens to that growth rate if the three largest customers start building their own training chips within two years?" — the output was different. Not necessarily correct, but substantive. It forced the agent to engage with a specific scenario, pull specific data, and reason about specific consequences. The output was useful because the input was useful.

This is the mirror principle: agents reflect the quality of your questions.

The same agent reflects a vague question back as an empty answer and a precise question back as a sharp one — the quality lives on the asker's side

The same agent reflects a vague question back as an empty answer and a precise question back as a sharp one — the quality lives on the asker's side

A mediocre question produces a mediocre answer. Not because the agent lacks capability, but because the question did not constrain the answer space enough to exclude platitudes. The agent is not being lazy. It is doing exactly what you asked — answering a question that has no specific answer with an answer that is not specifically wrong.

A precise question produces a precise answer. The precision is yours. The agent contributes speed, breadth, and computational accuracy. You contribute the angle, the constraint, the "what if" that makes the analysis non-obvious.

This is why the curriculum spent so much time on financial fundamentals before introducing fleet architecture. You cannot ask precise questions about a company's cash flow quality if you do not know what cash flow quality means. You cannot design a useful red-team prompt if you do not understand the thesis well enough to know where it is weakest. The fundamentals are not background knowledge. They are the raw material from which precise questions are built.

Where the mirror distorts

The metaphor has a limit, and it matters.

Agents do not simply reflect your question. They also add their own biases — toward consensus, toward recency, toward the data that is most available in their training. A perfectly precise question can still produce a subtly misleading answer if the agent's training data over-represents one narrative or under-represents a specific risk.

The mirror also flatters. An agent's output looks professional regardless of whether it is correct. It has clean formatting, confident language, and the appearance of thorough research. This is dangerous precisely because it feels like the mirror is showing you a smarter version of yourself, when it may be showing you a more confident version of consensus.

The discipline, then, is not just asking better questions. It is maintaining skepticism about the answers, even when — especially when — they confirm what you wanted to hear.

3. What compounds

Warren Buffett is often cited for the power of compound interest. The metaphor extends beyond money.

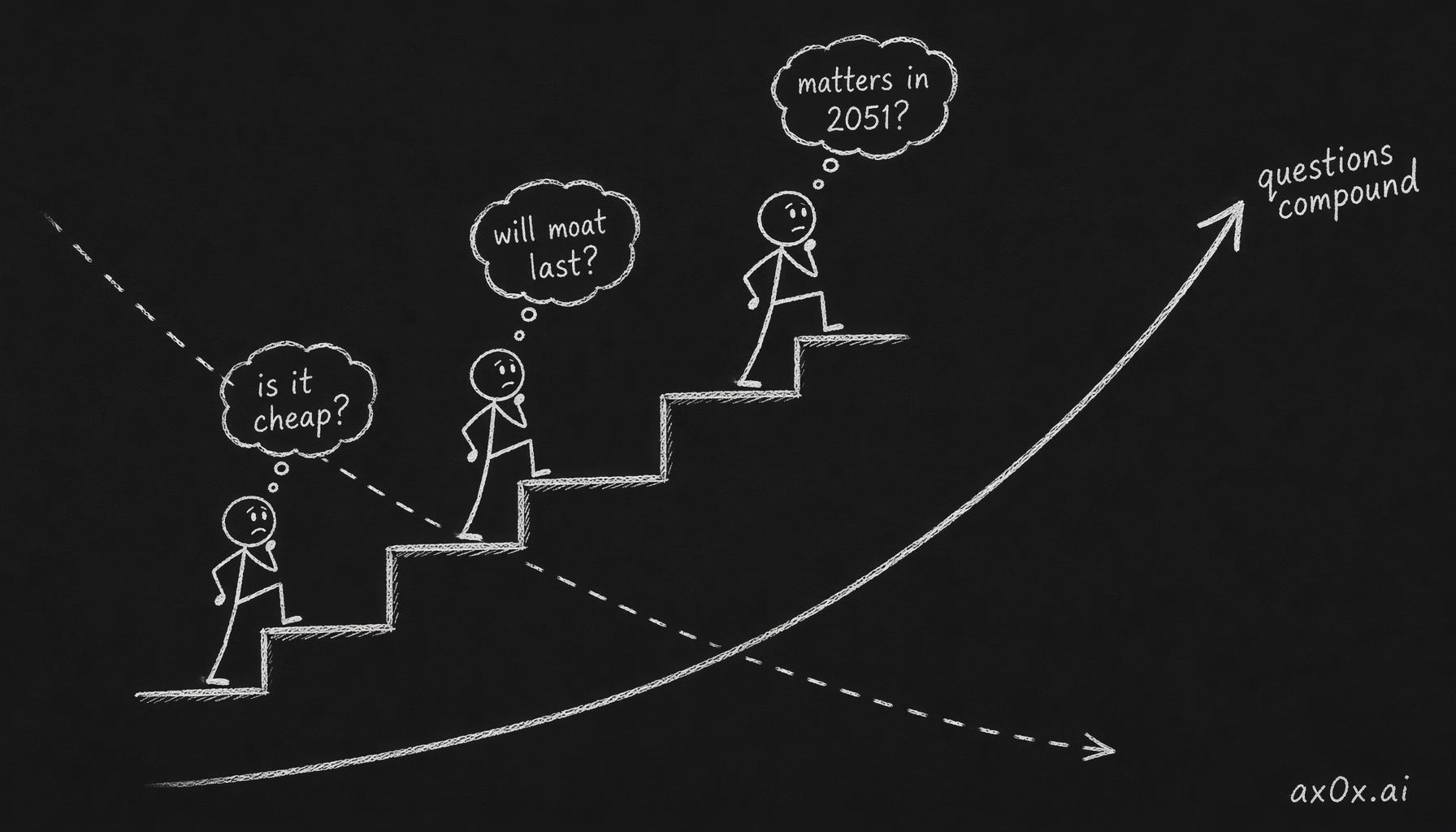

Over twenty-five years of investing, the thing that compounds is not your portfolio's returns. Returns are the output. What compounds is the input: your capacity to ask questions that other people are not asking.

Consider the progression. In year one, you ask: "Is this company cheap?" By year five, having been wrong several times, you ask: "Cheap relative to what? What am I assuming about growth, reinvestment, and competitive dynamics that could be wrong?" By year ten, you ask: "What does the market believe about this company, why does it believe that, and what would have to be true for the market to be wrong in a way I can identify before everyone else does?"

Information expires and methods depreciate, but the questions climb one level deeper each cycle — that rising capacity is the thing that actually compounds

Information expires and methods depreciate, but the questions climb one level deeper each cycle — that rising capacity is the thing that actually compounds

The questions get better because each mistake teaches you something that makes your next question more precise. The person who bought a "cheap" stock that turned out to be cheap for a reason learns to ask about the reason. The person who held through a drawdown because they confused conviction with stubbornness learns to distinguish between a thesis that is still valid under stress and a thesis that has quietly died.

This compounding is not accelerated by agents. Agents accelerate the analytical cycle — you can test more questions in less time — but they do not accelerate the learning that comes from being wrong with real stakes. That learning is physiological. It rewires your risk assessment in ways that reading about risk does not.

There is no shortcut. You cannot read your way to good judgment any more than you can read your way to good balance. The curriculum gave you the vocabulary and the frameworks. The compounding starts when you use them on real decisions, get some of them wrong, and pay enough attention to update your models honestly. Each update is a slightly better question. Over twenty-five years, slightly better questions compound into a fundamentally different understanding of what you are looking at.

Information does not compound

This is the counterpoint, and it is important.

More information does not make you a better investor. The marginal value of the five-hundredth research report on a company you already understand well is approximately zero. It may even be negative, because it creates the illusion of increasing certainty in an environment that is fundamentally uncertain.

Agents make it trivially easy to produce more information. You can run a twelve-agent research fleet on a single company and produce fifty pages of analysis in an afternoon. The question is whether those fifty pages changed any of your key assumptions. If they did not, the afternoon was wasted — worse than wasted, because it gave you the feeling of productivity without the substance.

The discipline of knowing when to stop researching and start deciding is one of the hardest skills in investing. It is also one that agents actively undermine, because producing more analysis feels like working, and stopping feels like giving up.

Howard Marks writes about the difference between first-level thinking ("this is a good company, therefore buy") and second-level thinking ("this is a good company, everyone knows it is a good company, therefore the price already reflects that, so the question is whether it is even better than everyone thinks"). The progression from first-level to second-level is not about having more information. It is about processing the same information with a better question.

4. The right to do nothing

The single most important investing skill is one that this curriculum cannot teach directly. It can only point at it.

The skill is the willingness to do nothing.

Most of your time as an investor should be spent not investing. Reading, learning, watching, updating your models — but not buying or selling. The reason is structural: genuinely good opportunities are rare. If you are finding them every week, you are not being selective enough, and the evidence across decades of market data confirms that high portfolio turnover correlates with lower returns for individual investors.

Buffett describes his approach as "waiting for the fat pitch." In baseball, a batter is not penalized for letting most pitches pass. In investing, there is no penalty for sitting in cash when nothing meets your criteria. The cost of inaction is opportunity cost — the return you might have earned — but the cost of action on a bad thesis is real loss, which is worse.

This is psychologically difficult for a specific reason: agents make action easy. When you have a fleet that can research any company in thirty minutes, the temptation to research, analyze, and act is constant. The tooling incentivizes activity. But investing rewards patience.

The curriculum taught you to build theses, run valuations, and stress-test ideas. It did not spend enough time on the most common correct conclusion of that entire process: "This is interesting, but I do not have enough conviction to act. I will revisit in six months."

That conclusion is not failure. It is discipline.

Circle of competence

Munger and Buffett both describe the "circle of competence" — the set of industries, business models, and dynamics that you genuinely understand well enough to have an edge.

The circle is small. For most individual investors, it encompasses their own industry, adjacent industries they follow closely, and perhaps one or two sectors they have studied deeply over years. Everything outside the circle is territory where your analysis is no better than consensus, regardless of how sophisticated your agent fleet is.

The temptation with agents is to expand the circle artificially. An agent can produce a semiconductor industry analysis that reads like it was written by a sector specialist. But reading a specialist-quality analysis does not make you a specialist. You lack the context to know what the analysis is missing, which assumptions are industry-standard-but-wrong, and what the experienced analysts in the room are thinking but not writing.

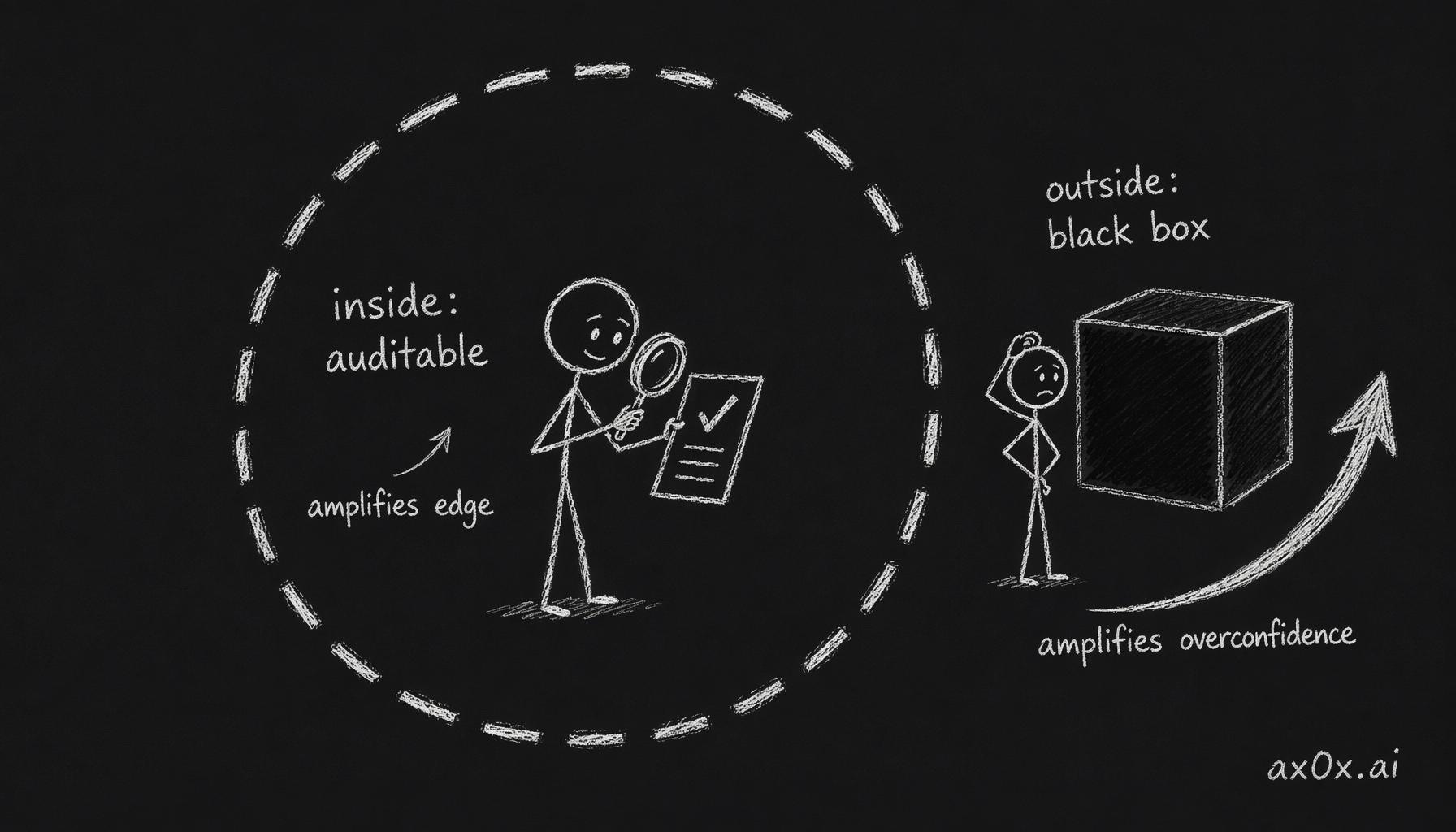

The honest move is to know where your circle ends and to be very careful about acting outside it. Inside your circle, agents amplify your edge — they speed up the work, cross-verify your assumptions, and catch errors in your reasoning. Outside your circle, agents amplify your overconfidence — they produce output that looks like expertise but is not grounded in the kind of deep understanding that makes expertise real.

Inside your circle the agent's output is auditable and amplifies your edge; outside it is a black box that amplifies overconfidence — so where the boundary sits matters more than how big the circle is

Inside your circle the agent's output is auditable and amplifies your edge; outside it is a black box that amplifies overconfidence — so where the boundary sits matters more than how big the circle is

Peter Lynch built his career on this principle. "Invest in what you understand" is not a platitude — it is a constraint on which opportunities you are qualified to evaluate. The constraint is what makes it powerful. Without the constraint, you are just another person with an opinion about everything and conviction about nothing.

Trade-off: patience as its own risk

There is a genuine cost to excessive patience.

Markets trend upward over long periods. Cash that sits uninvested has a real opportunity cost. The person who waited ten years for the "perfect pitch" while the S&P 500 compounded at 10% annually paid a steep price for their discipline.

The resolution is not to abandon patience but to be honest about its limits. Index funds exist. The decision to hold cash instead of a broad market index is itself an active bet — a bet that your future selective investments will outperform the index by enough to compensate for the time you spent waiting. For most individual investors, the honest answer is: keep most of your portfolio in low-cost index funds, and reserve a meaningful but bounded portion for the selective, thesis-driven investing this curriculum teaches. The curriculum is about building judgment, not about replacing diversification.

5. The twenty-five-year view

Imagine the investing landscape in 2051.

The agents will be better. Dramatically better. They will have access to data sources that do not exist today, process information at speeds that make 2026 capabilities look primitive, and produce analysis that is indistinguishable from — perhaps better than — what a human sector specialist produces today.

What will not change: someone has to decide. Someone has to weigh the analysis, assess the risks against their own circumstances, hold the position through volatility, and bear the consequences. The decision cannot be delegated, because the consequences cannot be delegated. Your risk tolerance, your time horizon, your financial obligations, your psychological response to losing money — these are yours, and no agent improvement changes that.

What also will not change: the market is a crowd of people making decisions based on their beliefs about the future. Better agents mean everyone's analysis improves, which means the analytical edge erodes, which means the remaining edges — patience, discipline, the willingness to be different from the crowd — become more valuable, not less.

This is the paradox of tool improvement in investing. The better the tools get, the less the tools matter relative to the person using them. When everyone has the same analytical capabilities, the differentiator is not capability. It is character.

Character in investing is specific. It is not about being brave or bold. It is about:

Intellectual honesty — the ability to change your mind when the evidence changes, without rationalizing why your original thesis was "sort of right."

Emotional discipline — the ability to hold a position you believe in when the price is moving against you, and to sell a position you love when your thesis is broken.

Humility — the recognition that you will be wrong regularly, that being wrong is not a personal failing but a structural feature of uncertainty, and that the goal is to be wrong in affordable ways.

These qualities are not taught. They are built through years of making decisions, observing the consequences, and being honest about the gap between what you expected and what happened.

The good news: the training ground is open. Before agents, practicing the full investment analysis cycle was expensive in either money (Bloomberg) or time (manual analysis). In 2026, you can run the full cycle — research, valuation, thesis, red-team, decision — on any public company in a few hours for the cost of a few dollars in API calls. You can repeat the cycle weekly if you want. Each cycle trains your judgment a little more. After fifty cycles, you will think about companies differently than you did after five. After five hundred, you will have something approaching the pattern recognition that used to take a decade at a fund to develop.

The bad news: there is no way to speed up the part where you put real money on the line, watch the market disagree with you for six months, and decide whether your thesis is wrong or the market is. That part takes however long it takes.

What Graham knew

Benjamin Graham published The Intelligent Investor in 1949. His core insight — that a stock is a fractional ownership in a business, not a lottery ticket — is seventy-seven years old and still the most important sentence in investment education.

Every tool since then — Bloomberg terminals, quantitative models, algorithmic trading, and now AI agents — has been layered on top of that insight without changing it. The tools change how you access information and how quickly you process it. They do not change what you are doing: buying a claim on future cash flows from a business, at a price, with a margin of safety that accounts for the possibility that you are wrong.

Graham also knew that the hardest part of investing was not analysis. He wrote: "The investor's chief problem — and even his worst enemy — is likely to be himself." The tools get better. The enemy stays the same.

Workshop — A letter without an agent

Time: 45–60 minutes. Tools: None. This is the only workshop in the curriculum where you do not use an agent. Output: A saved document, approximately 500 words.

Why no agent

Every other workshop in this curriculum used agents — to research, to red-team, to compute, to challenge. This one does not, because the question it asks is one that only you can answer, and running it through an agent would produce something articulate, well-structured, and entirely not yours.

The point of this exercise is to sit with your own thinking, without the comfort of a tool that makes your thinking sound more polished than it is.

Instructions

Write a letter from the version of yourself who exists twenty-five years from now — 2051. This future version has been investing for a quarter century. They have lived through at least two bear markets, several manias, a few investments they are proud of, and a few they would rather forget.

The letter is addressed to you, today, at the end of this curriculum.

It covers three things:

One: the thing you wish you had understood sooner about investing. Not a technique. Not "I wish I had learned about DCFs earlier." A deeper insight — about patience, about yourself, about the nature of making decisions under uncertainty. Something that took years of experience to internalize and that no curriculum could have taught you directly.

Two: the mistake you are most grateful for. A specific investment decision that went wrong and taught you something that made every subsequent decision better. What did you learn from it that you could not have learned any other way?

Three: what you would tell yourself about the relationship between tools and judgment. In 2051, the tools are unimaginably more powerful than what you have in 2026. What stayed the same? What matters more than you think it does right now?

Ground rules

- Do not research anything. Do not look up historical examples or quotes. Write from what you know and imagine right now.

- Write in the second person — "you" — as if the future version is speaking to the current version.

- 500 words, approximately. Not a minimum. Not a maximum. A target that keeps the letter tight enough to mean something.

- Save the document with today's date.

What to do with it

Seal it. Metaphorically or literally. Set a calendar reminder for one year from today.

When you open it in a year, you will know things about yourself as an investor that you do not know now. You will have made decisions — some good, some bad. The letter will tell you what you thought mattered before you had that experience. The gap between the letter and reality is the gap between framework and judgment. That gap is not a failure of the curriculum. It is the beginning of the real education.

The way is not a destination

The curriculum is over. The work is not.

You have frameworks for reading companies, building valuations, assessing risk, writing theses, and commanding agent fleets. Those frameworks will evolve as you use them. Some sections of this curriculum will seem naive to you in five years. That is the correct outcome — it means your judgment grew past the scaffolding.

What does not change is the underlying structure. You ask a question. You gather evidence. You form a judgment. You act on it or choose not to. You live with the consequences and update your understanding.

The tools will keep improving. The questions will keep getting harder. The only edge that lasts is the one that compounds: the habit of asking better questions than you asked last year.

Graham had it right seventy-seven years ago. You are buying a piece of a business. Everything else — the agents, the models, the fleet architecture — is in service of one judgment: is this business worth what you are paying, given what you do not know?

That judgment is yours. It always was.

This is the final chapter of the AI-Native Investor curriculum. The first chapter laid out the thesis: the barrier moved from tooling to judgment. Nine chapters later, the question is whether you built the judgment to match the tools. The answer will take years, not chapters. Start with the letter. Reopen it in a year.