Write It Down or It Isn't a Thesis

Chapter 7 of 10 in the AI-Native Investor curriculum.

In April 2020, you could find thousands of retail investors who "always believed in Tesla." By their own recollection, they had a thesis: electric vehicles would dominate, Tesla was the leader, Elon Musk was a generational founder. They held through the 2019 drawdown, the March 2020 crash, the skeptics. Their conviction was vindicated when the stock rose roughly 700% that year.

Except many of them did not have a thesis in 2019. They had a position. The thesis came later — assembled retroactively from outcome, stitched together by a memory that is neurologically incapable of remembering what you actually believed before reality proved you right. By 2021, those same investors held through the subsequent 70% decline because they "had conviction." They did. It was just conviction in a memory of a thesis they never wrote down.

This is not a character flaw. It is a feature of human cognition. Memory is reconstructive, not archival. Every time you recall a belief, you subtly rewrite it to be more consistent with what you know now. In investing, this means your thesis is always drifting — toward whatever narrative explains your current position, away from the uncomfortable parts that turned out to be wrong. You cannot feel this happening. It is like the hour hand on a clock: you never see it move, but it is never still.

Memory quietly rewrites your original call into hindsight, feeding the illusion you knew it all along

Memory quietly rewrites your original call into hindsight, feeding the illusion you knew it all along

The fix is simple and almost nobody does it. Write the thesis down. With specifics. With dates. With conditions under which you would change your mind. Then do not edit it — create a new version when your view changes.

This chapter teaches the structure, the psychology, and the agent workflow for doing exactly that.

What this chapter covers

- Why beliefs are not theses

- The six elements of a written thesis

- Why writing changes how you think

- Red-teaming: the agent as short seller

- Thesis version control — new versions, not patches

- The psychology you are fighting

- The agent's role: remind, not decide

- What formalization costs you

- Workshop: your first real thesis

1. Why beliefs are not theses

You have beliefs about every stock you own. You might believe Amazon will dominate cloud computing for the next decade, or that Nvidia's moat in AI chips is durable, or that a small biotech you bought has a promising pipeline. These beliefs feel like theses. They have a direction (bullish), a reasoning chain (cloud is growing, Amazon is the leader, therefore...), and emotional weight (you own the stock, so you care about being right).

They are not theses. They are beliefs, and the distinction matters for a specific, practical reason: beliefs are unfalsifiable as held in your head.

Ask yourself right now: what would have to happen for you to sell your largest position? If the answer is vague — "if the fundamentals deteriorated" or "if I lost confidence in management" — you do not have a thesis. You have a belief that will quietly reshape itself to accommodate whatever happens next. Fundamentals will "deteriorate" and you will find a reason it is temporary. You will "lose confidence" in management and then regain it when the stock recovers. The belief survives everything because it is never specific enough to die.

A thesis, by contrast, has a defined shape. It names specific conditions under which it would be wrong. It identifies what you are betting on and what you are betting against. It has a time horizon after which you evaluate the outcome regardless of whether the stock went up or down. Most importantly, it exists as a document with a date on it — a document you cannot gaslight.

Warren Buffett has described his approach to investment decisions as requiring the ability to write a short essay explaining why a business is worth buying at its current price. Not a spreadsheet, not a model — a written argument. If you cannot write the essay, you do not understand the investment well enough to make it. The discipline of writing forces a level of clarity that holding a belief in your head does not require.

Belief drift in practice

Here is how belief drift works. You buy Company X because you believe its new product line will capture 15% market share within three years. Nine months later, the product launch is delayed. The stock drops 20%. You tell yourself that the thesis is still intact — delays happen, the product is still strong. Fair enough. Twelve months later, the product launches but captures 4% market share in the first year, tracking well below your original 15% target. The stock is flat. You tell yourself that market adoption takes time, and the competitive landscape shifted, and really the thesis was always about the company's long-term platform potential, not any single product.

Notice what happened. The thesis mutated three times. The original thesis — 15% market share in three years — is failing. But because it was never written down with those specific numbers, you do not experience it as a failure. You experience it as an evolution of your thinking. The belief adapted to survive. Your memory cooperated.

Now imagine you had written down, on the day you bought: "Bull case: new product captures 15% market share within 3 years. If market share is below 8% after 18 months, reassess position. If product launch is delayed more than 6 months, reassess position." The delay happens — you reassess. The market share tracks below 8% at the 18-month mark — you reassess. You might still hold the position. But the reassessment is forced, conscious, deliberate. You are making a new decision, not drifting into one.

That is the difference between a belief and a thesis. A belief accommodates. A thesis confronts.

2. The six elements of a written thesis

A thesis is not a bull case paragraph. It is a structured document with six elements, each of which forces a specific kind of clarity. If any element is missing, the thesis has a gap you will exploit later — unconsciously — to avoid facing disconfirming evidence.

Element 1: Catalyst — why now?

The catalyst answers: why does this investment make sense today rather than six months ago or six months from now? A stock can be a great company and a bad investment if the timing is wrong. The catalyst is what makes the timing arguably right.

Catalysts come in several forms. An earnings inflection — the company's margins are about to expand because a major cost is falling off. A product cycle — a new product is about to launch that addresses a market the company has not served before. A sentiment reset — the market has overcorrected on bad news, and the stock is priced for a disaster that is unlikely to materialize. A structural change — a regulation is shifting, a competitor is exiting, a supply chain is reconfiguring.

The discipline of naming a catalyst prevents the most common amateur investing mistake: buying a good company at any price because you like it. Costco is a wonderful company. It is rarely a wonderful investment at the moment you feel like buying it, because everyone else also knows it is a wonderful company, and the price reflects that. A catalyst is what separates "I like this company" from "I believe the market is wrong about this company right now, for this specific reason."

Trade-off: Requiring a catalyst biases you toward event-driven investing and away from long-duration compounding bets where there is no specific "why now" — there is only "this company will be worth substantially more in ten years." Some of the best investments have no identifiable catalyst at purchase. Buffett's purchase of Coca-Cola in 1988 did not have a catalyst in the traditional sense; he simply believed the brand's earnings power was underpriced. If your thesis is genuinely long-duration, name that explicitly: "The catalyst is the absence of a catalyst — the market is pricing this for stagnation and I believe it will compound." That is a valid catalyst. "I just like the stock" is not.

Element 2: Moat — why won't this get competed away?

The moat answers: assuming the catalyst plays out, why will this company capture the value rather than losing it to competitors? A growing market with no moat is not an investment thesis — it is a bet that every competitor will win, which is a bet that usually loses.

Moats take recognizable forms. Network effects — each additional user makes the product more valuable, which attracts more users, which creates a loop competitors cannot easily enter. Switching costs — customers have invested so much in the product (data, training, integrations) that moving to an alternative is expensive and risky. Scale economics — the company's cost structure improves with volume in ways that smaller competitors cannot match. Intangible assets — brands, patents, regulatory licenses that legally or psychologically prevent competition.

The moat element of your thesis should name which type of moat you believe exists and — critically — how durable it is. A network effect that can be replicated by a well-funded competitor in two years is a weaker moat than a regulatory barrier. Your thesis needs to be honest about moat durability, because this is where most bullish theses quietly fudge the details.

Element 3: Management — can these people execute?

Management answers: even if the market opportunity is real and the moat exists, can the specific humans running this company capitalize on it?

This is the hardest element to evaluate from public data. An agent can pull management bios, compensation structures, insider buying and selling patterns, and track records at prior companies. These are useful data points. But management quality is ultimately a judgment call that incorporates soft signals: how management communicates during earnings calls (are they evasive about bad news?), whether they under-promise and over-deliver or vice versa, whether their capital allocation decisions make long-term sense or optimize for short-term stock price.

Include this in your thesis not as a rating ("management is strong") but as specific observations: "CEO has allocated capital conservatively for five years, insider buying increased during the last drawdown, compensation is tied to free cash flow growth rather than revenue growth." If you cannot point to specific evidence, your management assessment is a vibe, and vibes drift.

Element 4: Valuation frame — what are you paying?

The valuation frame connects your thesis to price. It answers: at today's price, what does the market believe about this company, and how does that differ from what I believe?

This is not asking for a precise DCF output. It is asking you to articulate the gap between what the market is pricing in and what your thesis implies. If a company trades at 15x earnings and your thesis implies earnings will double in three years, the gap is clear: the market does not believe earnings will double. Your thesis is a bet that they will. If the company trades at 50x earnings and your thesis also implies earnings doubling in three years, the gap is narrower — the market might already agree with you, and you are paying for a thesis that is already priced in.

Chapter 5 covered valuation in detail — how every input in a DCF is a story choice, and how sensitivity analysis reveals which assumption your valuation secretly depends on. The valuation frame element of your thesis does not require you to run a fresh DCF. It requires you to name the story the market is currently telling about this company, name how your story differs, and acknowledge what you are paying for the right to be different.

Element 5: Kill criteria — when are you wrong?

Kill criteria are the most important element of the thesis and the one most investors skip entirely. They answer: what specific, observable conditions would force you to conclude that your thesis is broken?

Kill criteria are not stop losses. A stop loss says "sell if the price drops 15%." Price movement alone tells you nothing about whether your thesis is correct. A stock can drop 30% because the market is panicking while every element of your thesis remains intact. A stock can rise 50% while the fundamental thesis is deteriorating, carried by momentum and narrative.

Kill criteria are tied to the thesis elements, not to price. If your catalyst was margin expansion, a kill criterion might be: "If gross margins have not expanded by at least 200 basis points within two quarters, reassess." If your moat was network effects, a kill criterion might be: "If monthly active user growth declines for three consecutive quarters, reassess." If your management assessment depended on capital discipline, a kill criterion might be: "If the company makes an acquisition above $2 billion that is outside their core competency, reassess."

Notice the word "reassess" rather than "sell." Kill criteria trigger a forced re-examination, not an automatic exit. You might reassess and conclude the thesis is still valid for a new reason. That is fine — but now you have a new thesis, not a drifted belief. You are making a conscious decision, recorded with a new date, rather than sleepwalking into a position you no longer have a reason for.

Trade-off: Kill criteria can be gamed by your own psychology. If you set them too loosely ("reassess if something really bad happens"), they never trigger. If you set them too specifically ("reassess if Q3 revenue misses by more than 2%"), they trigger on noise. The right granularity sits between these extremes and takes practice to calibrate. Expect your first several sets of kill criteria to be either too loose or too tight. The value is in having them at all, not in getting them perfect on the first try.

Element 6: Time horizon — when do you evaluate?

The time horizon answers: how long does this thesis need to play out? At what point do you assess whether it worked, independent of where the stock price is?

A thesis without a time horizon is a belief wearing a suit. "I think this company will do well" is not a thesis. "I believe this company's cloud margins will reach 30% within 18 months, driven by the shift to higher-margin enterprise contracts" is a thesis with a clock on it. At the 18-month mark, you check: did margins reach 30%? If yes, the thesis played out — decide whether a new thesis justifies continuing to hold. If no, the thesis failed — decide what that means.

The time horizon also determines which risks are relevant. A three-month thesis is dominated by sentiment, positioning, and near-term earnings surprises. A three-year thesis is dominated by business fundamentals, competitive dynamics, and management execution. A ten-year thesis is dominated by secular trends, moat durability, and capital allocation. If your time horizon does not match the type of evidence you are citing, you have an internal contradiction.

Howard Marks has written extensively about the relationship between time horizon and investment discipline. Short time horizons amplify noise. Long time horizons require patience that most people do not have — not because they lack character, but because the feedback loop is too slow to reinforce good behavior. Choose the time horizon that matches your actual temperament, not the one that sounds most sophisticated. A well-executed twelve-month thesis is more valuable than a poorly-held ten-year thesis that you abandon after six months of underperformance.

3. Why writing changes how you think

There is a widespread assumption that writing a thesis is simply recording what you already think — that the thinking happens first and the writing is transcription. This is wrong in a way that matters for investing.

Writing is not transcription. Writing is a thinking process that forces completeness, coherence, and confrontation with gaps in your reasoning. When you hold a belief in your head, it is fluid. It does not need to be internally consistent because you never examine all of it at once. You consider the bull case in one moment and the risk in another moment, and the two moments do not have to reconcile. Writing forces them onto the same page, literally, where contradictions become visible.

Try this experiment: before writing your thesis, ask yourself how confident you are in your investment on a scale of 1 to 10. Then write the thesis using the six elements. Then ask yourself the same question. Most people report lower confidence after writing — not because the investment got worse, but because writing exposed gaps they were not aware of. That drop in confidence is not a loss. It is information. You were overconfident before. Now you are calibrated more accurately.

Benjamin Graham argued that the margin of safety was the central concept of investment — the idea that you should buy at a price that leaves room for your analysis to be wrong. Writing a thesis is the mechanism by which you discover how much room you need. You cannot assess your margin of safety if you do not know where your analysis might fail. Writing forces you to enumerate the failure points.

Writing as a commitment device

There is a second, subtler benefit. A written thesis is a commitment device against future rationalization.

In behavioral economics, a commitment device is a mechanism that restricts your future choices to prevent you from acting against your own interests. Odysseus tying himself to the mast to resist the Sirens is the classic example. A written thesis functions the same way. When the stock drops and the temptation to rationalize is strongest — "the market just doesn't understand," "this is temporary," "the thesis evolved" — the written document sits there, unchanged, forcing you to contend with what you actually believed when you made the decision.

You do not have to obey the document. You are allowed to change your mind. But changing your mind looks different when you have to explicitly cross out what you wrote and write something new, with a new date, versus when you simply let the old belief fade and the new belief take its place. The friction is the point. It is the difference between a deliberate course change and an unconscious drift.

4. Red-teaming: the agent as short seller

You have a written thesis. It looks good. You feel confident. This is the moment of maximum danger.

Confidence after writing a thesis is often a symptom of having written the thesis you wanted to write rather than the thesis the evidence supports. The six elements provide structure, but structure does not guarantee honesty. You can write a beautifully structured thesis that is wrong because every element was filled in with the most optimistic plausible interpretation.

This is where red-teaming enters. And this is where agents provide a specific, practical advantage that is hard to replicate with human discipline alone.

The short-seller frame

Short sellers — investors who profit when a stock declines — have a structurally different incentive from you. You own the stock. You want the thesis to be right. A short seller wants to find the flaw in your thesis — the hidden liability, the deteriorating moat, the management team that is good at storytelling and bad at execution, the valuation that only works if you squint at the growth assumptions.

Real short sellers — the good ones, like the analysts behind Muddy Waters or Hindenburg Research — are ruthlessly specific. They do not say "this stock is overvalued." They say "this company's accounts receivable have grown 3x faster than revenue for four consecutive quarters, which in our experience of covering companies in this sector has been a leading indicator of aggressive revenue recognition that eventually reverses." That level of specificity is what makes a short-seller attack useful.

You can instruct an agent to play this role. The key is framing. If you tell an agent "what are the risks of this investment?", you will get a polite list of generic risks — competition, regulation, macroeconomic headwinds. This is useless. Every investment has these risks. Listing them teaches you nothing.

Instead, frame the agent as a short seller with a position against you. Give it your written thesis — all six elements — and tell it to write the three strongest arguments for why your thesis will fail. Not generic risks. Specific attacks on specific elements. If your catalyst is margin expansion, the short seller should argue why margins will not expand — with evidence, not vibes. If your moat is network effects, the short seller should identify the specific conditions under which the network effects could weaken or reverse.

The attack-and-iterate loop

The first round of attacks will probably land. Your thesis will have genuine weaknesses, and the agent-as-short-seller will find them. This is useful but not yet valuable. The value comes from the iteration.

Take the three attacks. For each one, do one of three things:

Concede. The attack is right. Your thesis has this weakness. Revise the thesis to acknowledge it, and either adjust your position sizing to account for the risk or add a kill criterion that will force you to reassess if this specific weakness materializes.

Counter. The attack identifies a real risk, but you have evidence or reasoning that mitigates it. Write the counter-argument into the thesis. Be specific — "I acknowledge this risk and believe it is mitigated because [specific evidence]." Now your thesis is more robust because it has addressed the objection rather than ignored it.

Dismiss. The attack misses the mark — it is based on a misunderstanding of the business, outdated data, or a generic concern that does not apply. Dismiss it explicitly and state why.

After the first revision, run the red team again. Give the agent your revised thesis and ask for three new attacks — not the same ones. The attacks should get harder to construct. If the second round's attacks are as strong as the first round's, your thesis had more holes than you thought. If the second round's attacks are weaker, reaching for increasingly improbable scenarios, you are getting somewhere.

The loop terminates when the attacks become implausible — when the short seller has to stretch into "what if the entire sector is disrupted by a technology that doesn't exist yet" or "what if management commits fraud." Those are real risks in the literal sense, but they are not falsifying your thesis. They are tail risks that you account for through position sizing, not thesis design.

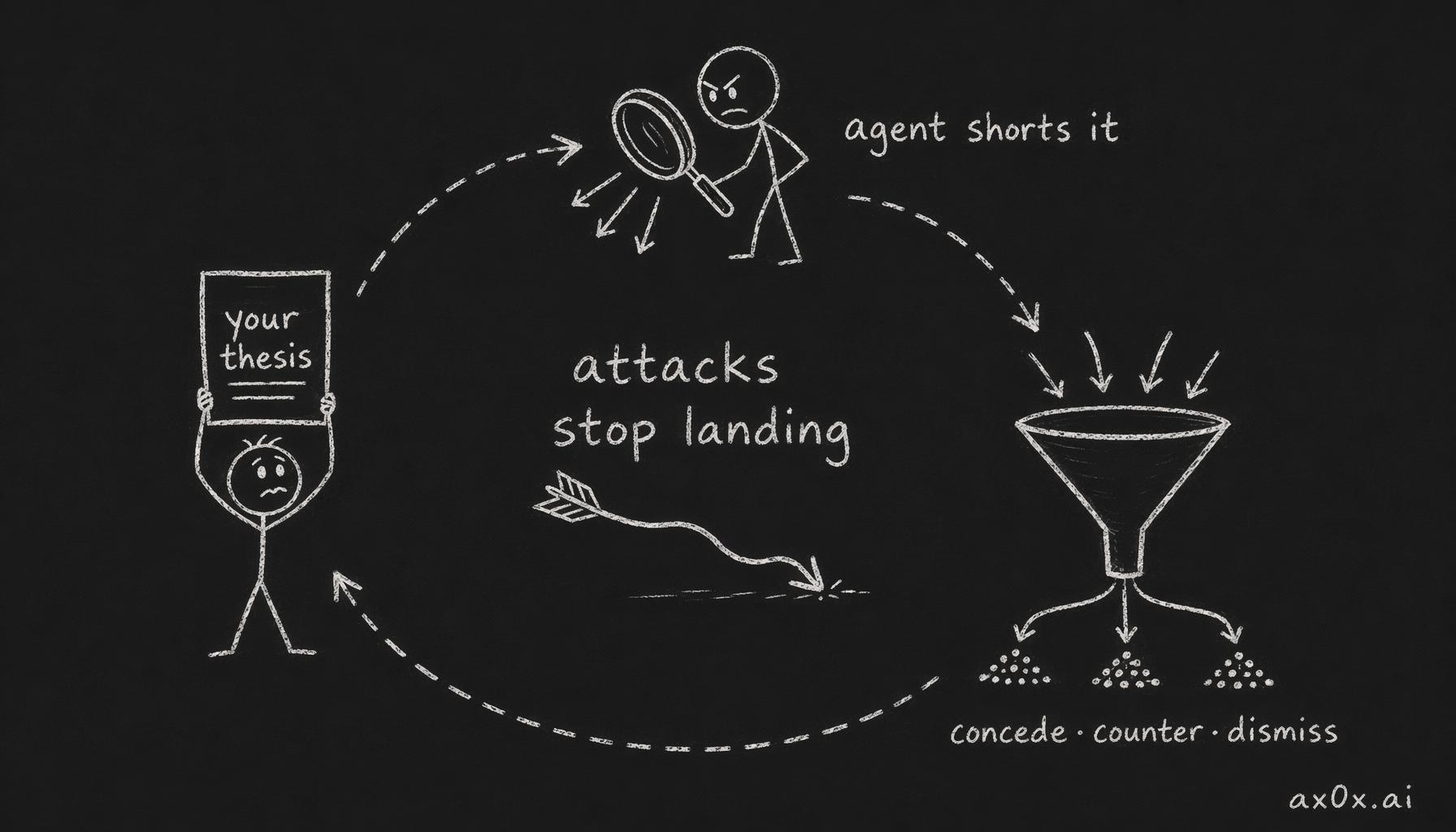

The agent-as-short-seller loop: attack the thesis, concede/counter/dismiss, revise, repeat until the attacks stop landing

The agent-as-short-seller loop: attack the thesis, concede/counter/dismiss, revise, repeat until the attacks stop landing

Three to four rounds is typical for a thesis of moderate complexity. If you are still fielding strong attacks after five rounds, the thesis might not be defensible. That is also valuable information.

What the agent is actually good at here

The agent's strength in red-teaming is not imagination — it is thoroughness. You, as the thesis writer, have blind spots created by your own conviction. There are avenues of attack you do not consider because considering them feels uncomfortable. The agent does not have this discomfort. It will methodically test each element of your thesis against each plausible failure mode without flinching.

The agent's weakness is creativity. It will find the attacks that follow from conventional analysis — the ones a diligent analyst would surface. It will not find the truly surprising risk — the one that comes from a structural shift nobody is discussing, or from a connection between two unrelated developments that changes the game. Those attacks come from human insight, and they are rare even among professional short sellers.

Use the agent for systematic coverage. Keep the idiosyncratic insight for yourself.

Trade-off: Agent red-teaming can create false confidence in the opposite direction — if the agent cannot find strong attacks, you might conclude your thesis is bulletproof. It is not. The agent's inability to attack your thesis might mean the thesis is strong, or it might mean the real risk is outside the agent's frame of reference. The red-team loop is a floor, not a ceiling. It catches the obvious weaknesses. The non-obvious ones require judgment, sector knowledge, and pattern recognition that accumulate over years of paying attention.

5. Thesis version control — new versions, not patches

Your thesis will change over time. This is not a failure — it is inevitable. Companies report earnings. Competitors enter markets. Macroeconomic conditions shift. Management makes decisions you did not anticipate. The world moves, and a thesis that does not respond to new information is dogma, not analysis.

The question is how to manage change without losing accountability.

The answer is versioning. When your thesis changes, you create a new version with a new date. You do not edit the old version. You do not delete it. You preserve the original alongside the revision, so that you always have a record of what you believed, when you believed it, and what changed.

What a version looks like

Version 1.0 is the thesis you wrote when you initiated the position — the full six elements, dated, after red-teaming.

Version 1.1 is a minor revision. Something changed that modifies one element without invalidating the core thesis. For example: you wrote your thesis on a cloud infrastructure company with a catalyst of margin expansion. The company reports earnings and margins expanded, but less than you expected. Your catalyst is partially validated. You revise the time horizon or adjust the kill criteria, note the new data, and date the revision.

Version 2.0 is a major revision. Something changed that alters the core thesis. The company you invested in for its enterprise cloud business announces a pivot to consumer AI. The moat element changes. The catalyst changes. The valuation frame changes. This is not a tweak — it is a new thesis. Maybe you still hold the position, but you are holding it for new reasons that should be explicitly stated and stress-tested from scratch.

Why patches are dangerous

The instinct when your thesis encounters disconfirming evidence is to patch it — add a footnote, adjust an assumption, move a goalpost. Patching feels reasonable. "My thesis was mostly right, I just need to account for this new development." The problem is that a series of reasonable patches can transform your thesis into something unrecognizable from the original — and because each individual patch felt small, you never noticed the total drift.

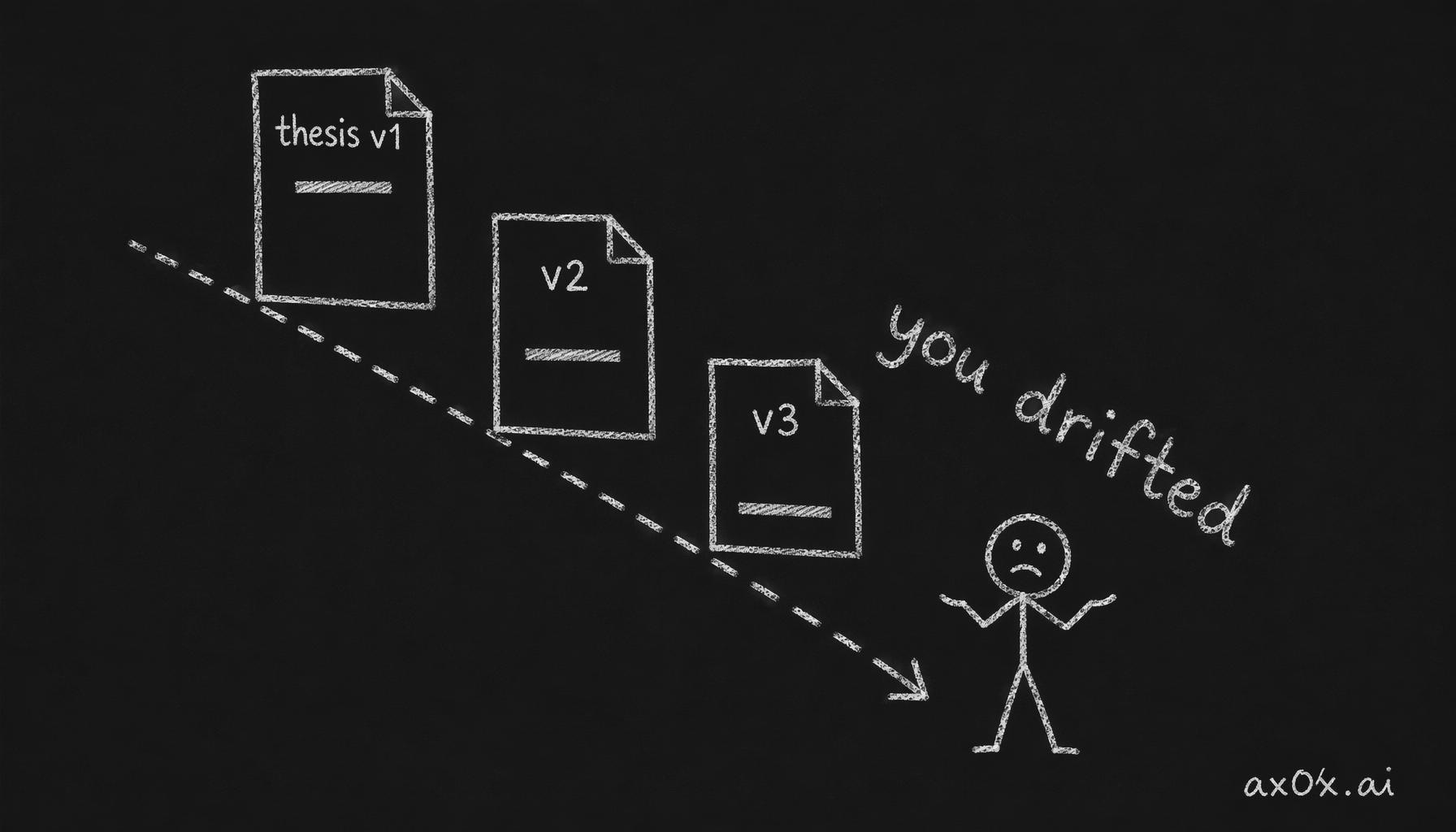

A run of reasonable patches quietly lowers the same goalpost version after version until the thesis is unrecognizable — you drifted

A run of reasonable patches quietly lowers the same goalpost version after version until the thesis is unrecognizable — you drifted

This is the ship of Theseus problem applied to investment convictions. If you patch the catalyst, then patch the moat assessment, then patch the time horizon, then patch the kill criteria — is it still the same thesis? Functionally, no. But psychologically, it feels like it is, because you never made a sharp break. You drifted.

Versioning forces sharp breaks. When enough has changed that you need a new version, you sit down and write the new thesis from scratch. You look at the original. You see how far you have moved. You make a conscious judgment about whether the new thesis is better or whether you are rationalizing. This confrontation is uncomfortable. It is supposed to be.

The 90-day review

A practical rhythm: review your thesis every 90 days, or after any earnings report or material event, whichever comes first. The review has three possible outcomes:

Reaffirm. Nothing has changed materially. The thesis holds. Note the review date and move on.

Revise. Something has changed that requires a minor version update. Write the revision, date it, explain what changed and why.

Retire. The thesis is broken. One or more kill criteria were triggered, or the cumulative weight of changes means you no longer have conviction in the core argument. This does not necessarily mean sell — you might write a new thesis that justifies the position for different reasons. But you need to be honest that the original thesis died, and you need a new one to continue holding.

The 90-day cycle aligns with quarterly earnings reports for most public companies. It is frequent enough to catch drift and infrequent enough to avoid reactive tinkering based on daily noise.

Trade-off: Formal versioning can become its own form of procrastination. If you spend more time maintaining thesis documents than developing investment judgment, the process is defeating its purpose. The document is a tool for accountability, not a product in itself. A thesis review should take 30 to 60 minutes per position. If it takes longer, you are either over-engineering the documentation or discovering that your thesis has bigger problems than you thought — in which case the time is well spent.

6. The psychology you are fighting

The six-element thesis, the red-teaming loop, and the versioning discipline are all designed to counteract specific cognitive biases that reliably destroy investment returns. Understanding these biases is not optional — it is the reason the entire system exists.

Confirmation bias

Confirmation bias is the tendency to seek, interpret, and remember information that confirms your existing beliefs while ignoring or discounting information that contradicts them. In investing, this is the mechanism that transforms a neutral earnings report into evidence that you are right.

A company reports flat revenue. If you are bullish, you interpret flat revenue as "resilience in a tough market." If you are bearish, you interpret it as "stalling growth." The data is the same. The interpretation is driven by prior belief. And the dangerous part is not the interpretation itself — it is that the interpretation feels objective to the person doing it. You genuinely believe you are looking at the evidence neutrally. You are not.

The written thesis combats confirmation bias by forcing you to name what you expected before the evidence arrives. If your thesis says "I expect revenue to grow 12% year-over-year," and revenue comes in flat, the discrepancy is clear. You cannot retroactively claim you expected resilience. The document does not lie.

The red-teaming loop combats confirmation bias by structurally forcing you to consider the bear case. You do not have to seek out disconfirming evidence on your own — you assign an agent to do it. The agent does not share your emotional investment in being right, and the quality of its attacks does not degrade when the evidence is uncomfortable.

Loss aversion

Loss aversion — the finding that losses feel roughly twice as painful as equivalent gains feel pleasant — distorts thesis discipline in two specific ways.

First, it makes you reluctant to acknowledge when a thesis is broken. Acknowledging a broken thesis means acknowledging a loss, which triggers pain. So you patch the thesis instead of retiring it, because patching allows you to maintain the narrative that you have not lost — you are just in a different phase of the investment. The versioning discipline combats this by making the choice binary: either the thesis holds as written, or you create a new version. There is no middle ground where you pretend nothing changed.

Second, loss aversion makes you sell winners too early and hold losers too long — a pattern so common it has a name (the disposition effect, documented by Terrance Odean). You sell the stock that went up 40% because locking in a gain feels good, and you hold the stock that is down 30% because selling would make the loss real. The kill criteria combat this by tying your sell decisions to thesis validity rather than to gains and losses. If the thesis holds, you hold — regardless of whether you are up or down. If the kill criteria are triggered, you reassess — regardless of whether you are up or down.

Sunk cost fallacy

Sunk cost fallacy is the tendency to continue an endeavor because of previously invested resources (time, money, effort) rather than on the basis of future value. In investing, this manifests as: "I've held this for two years and done so much research — I can't sell now."

The sunk cost fallacy is particularly insidious because it masquerades as discipline. "I'm a long-term investor, I don't panic sell" sounds exactly like "I've invested too much into this thesis to admit it's wrong." The difference is whether the long-term holding is based on a thesis that still holds or on the discomfort of admitting you were wrong.

The versioning discipline exposes sunk cost thinking by forcing periodic confrontation with the thesis as it stands today — not as it stood when you bought. If Version 3.0 of your thesis bears no resemblance to Version 1.0, you are not a long-term investor in the same thesis. You are a serial rationalizer holding a position out of inertia.

Narrative fallacy

Nassim Taleb identified the narrative fallacy — our tendency to construct coherent stories from random events and then mistake the story for causation. In investing, this shows up as hindsight narratives: "Of course Tesla succeeded — electric vehicles were inevitable, battery costs were declining, Musk is a visionary." This narrative is constructed after the fact. In 2017, the narrative was equally coherent in the other direction: "Tesla will fail — they can't manufacture at scale, they're burning cash, the legacy automakers will crush them once they commit to EVs."

The written thesis with a date on it is a weapon against narrative fallacy. It freezes your narrative at a specific moment in time, before the outcome is known. When you review it later, you can compare what you actually believed against what happened — and more importantly, against what you now remember believing. The gap between the document and your memory is the narrative fallacy in action. Over time, observing this gap calibrates your confidence and teaches you how unreliable your own recollection is.

7. The agent's role: remind, not decide

Throughout this chapter, the agent has appeared in two roles: red-teamer and reviewer. Both are important. But there is a third role that is perhaps the most valuable for thesis discipline, and it is the simplest one: the agent as memory.

You wrote a thesis. You filed it. Three months pass. An earnings report comes out. You read the headlines, glance at the numbers, and form an opinion. At this point, you have probably already forgotten the specific details of your own thesis. You remember the direction (bullish) and the general shape (something about margins and management), but the specific kill criteria, the specific time horizon, the specific valuation frame — those have faded.

Before you form a judgment about the earnings report, ask the agent to read your thesis back to you. Not summarize it — read it. Then ask the agent to compare the earnings data against each of the six elements. Which elements were confirmed? Which were challenged? Were any kill criteria triggered?

This is not asking the agent to make a decision. It is asking the agent to do something humans are bad at: accurately recall a specific document and systematically compare it against new data. You are using the agent as external memory — a memory that does not drift, does not rationalize, and does not forget the uncomfortable parts.

The decision is still yours. The agent cannot tell you whether to hold, sell, or buy more. It does not know your financial situation, your risk tolerance, your other positions, your tax considerations, or your psychological state. It can tell you whether the evidence is consistent with the thesis you wrote. What you do with that information is the judgment that Chapter 2 identified as fundamentally human — the judgment that agents cannot replace.

Designing a review prompt

When you use an agent for thesis review, specificity matters. A prompt like "what do you think of my thesis given these earnings?" will produce a vague response. Instead, structure the review as a comparison.

Give the agent three things: your thesis document (the current version, with all six elements), the new information (earnings report, news event, competitor action), and a specific instruction — compare each thesis element against the new information and flag any element where the new information is inconsistent with the thesis.

The output should be a structured comparison, element by element. Catalyst: the thesis expected X, the earnings show Y, consistency assessment. Moat: the thesis assumed network effects are strengthening, the user metrics show Z, consistency assessment. And so on.

This is mechanical work. It is exactly the kind of work agents do well. And it is exactly the kind of work that humans skip because reading your own thesis against new data is boring and occasionally painful.

What the agent should never do

The agent should never tell you whether to buy or sell. This is worth stating explicitly because the temptation to ask is strong, and agents will answer if you ask — they will produce a confident-sounding recommendation that is based on the same consensus assumptions that make agent-generated analysis dangerous in the first place.

The division of labor from Chapter 1 applies here: agents handle the analytical grunt work, and you handle the judgment. For thesis discipline, the grunt work is recall, comparison, and systematic red-teaming. The judgment is: given this comparison, do I still believe this thesis? That question has no right answer that an agent can compute.

8. What formalization costs you

This chapter has argued that written, versioned theses with kill criteria are strictly better than holding beliefs in your head. That argument is mostly correct, but the costs of over-formalization are real and should be stated honestly.

Rigidity

A thesis with specific kill criteria can make you too mechanical. Markets are complex adaptive systems. Sometimes the right response to disconfirming evidence is not "trigger the kill criterion and reassess" but "this evidence is noise and I should ignore it." The challenge is that this response sounds exactly like rationalization — and sometimes it is.

Kill criteria need to be revisited periodically, not because your discipline is weak, but because the world changes in ways you did not anticipate when you wrote them. A kill criterion that made sense in a stable macroeconomic environment might not make sense during a financial crisis, when every company's margins are under pressure for reasons unrelated to the thesis. Slavish adherence to criteria written in a different regime is not discipline — it is rigidity.

The mitigation: when you override a kill criterion, write down why. If you are overriding kill criteria regularly, that is a signal that either your criteria are poorly calibrated or you lack the discipline to follow them. Both problems are diagnosable if you have the documentation.

Analysis paralysis

The six-element thesis, the red-teaming loop, the versioning system — taken together, these could become a reason to never make a decision. If you need a perfect thesis before taking a position, you will never take a position, because a perfect thesis does not exist. At some point, you have to decide with incomplete information, knowing that some of your assumptions are wrong and that you will learn which ones only after committing capital.

The system in this chapter is designed to improve the quality of decisions at the margin, not to eliminate uncertainty. If you find yourself endlessly revising your thesis and never acting, the system is being used as a procrastination tool rather than a decision tool. Two to three rounds of red-teaming is enough. A thesis that survives three rounds of serious attack is ready to be acted on, with appropriate position sizing from Chapter 6.

Formality fatigue

Maintaining versioned thesis documents for every position takes time. If you have ten positions, and each one requires a 90-day review, and each review takes 30 to 60 minutes, you are spending 5 to 10 hours per quarter on thesis maintenance. For a professional fund manager, this is table stakes. For an individual investor managing a portfolio alongside a full-time job, it is a meaningful time commitment.

The practical advice: you do not need a formal thesis for every position. Index funds and diversified holdings that you intend to hold for decades do not need six-element theses — they need a simple rationale ("I believe in long-term equity returns and I'm diversified") and nothing more. Formal theses are for individual company bets where you are making a specific judgment that differs from market consensus. If you have two or three of those, the time commitment is manageable. If you have fifteen, you have too many active theses — and the solution is concentration, not more documentation.

Workshop — Your first real thesis

Time: 60–90 minutes. Tools: Any AI agent. The document you saved in the Chapter 1 workshop. Output: A dated thesis document with six elements and at least one round of red-teaming.

Instructions

Step 1 — Reopen your Chapter 1 document. Find the bull case, bear case, and the sentence you wrote: "The claim I disagree with most strongly is __________, and I believe this because __________." Read it. Notice whether you remember it accurately or whether your memory has already drifted. That drift — however small — is what this chapter is about.

Step 2 — Write a 200-word thesis. Using the same company from Chapter 1, write a thesis that addresses all six elements:

- Catalyst: Why is now the right time? What specific event or trend creates an opportunity the market is not fully pricing?

- Moat: What structural advantage does this company have that prevents competitors from capturing the value even if the market opportunity is real?

- Management: What specific evidence — not vibes — supports your assessment of whether this team can execute?

- Valuation frame: At today's price, what is the market pricing in? How does your thesis differ from that implied story?

- Kill criteria: Name two to three specific, observable conditions that would force you to conclude the thesis is broken. These must be falsifiable — vague warnings like "if fundamentals deteriorate" do not count.

- Time horizon: When will you evaluate this thesis against reality? Pick a date.

Two hundred words is tight. That constraint is deliberate. If you cannot state the thesis in 200 words, you do not yet understand it well enough. Every word should be load-bearing.

Step 3 — Red-team. Give your 200-word thesis to an agent with this framing: "You are a short seller with a position against this company. Read this thesis and write the three strongest, most specific arguments for why this thesis will fail. Do not list generic risks. Attack the specific elements — the catalyst, the moat, the management assessment, the valuation frame. Use evidence where possible."

Read the three attacks. For each one, decide: concede, counter, or dismiss. Write your response next to each attack.

Step 4 — Revise. Rewrite your thesis incorporating the concessions and counter-arguments from Step 3. The revised thesis should be stronger — it should address the legitimate attacks and explain why the remaining attacks miss. If the revised thesis is weaker — if the attacks exposed fatal problems you cannot resolve — that is the most valuable outcome of this workshop. You just saved yourself from a bad investment.

Step 5 — Second round. Give the revised thesis to the agent with the same short-seller framing. Ask for three new attacks — not the ones already addressed. If the new attacks are weaker and more speculative, your thesis is solidifying. If they are equally strong, you have more work to do — or the investment genuinely does not have a defensible thesis.

Step 6 — Save with a date. Save the final version with today's date and "v1.0" in the title. This is the document you will compare against reality in 90 days — or when the next material event occurs, whichever comes first.

Step 7 — Note your confidence level. On a scale of 1 to 10, how confident are you in this thesis right now? Write the number at the bottom of the document. You will check this number when you do your first 90-day review. Most people find their confidence at the 90-day mark differs meaningfully from what they recorded on day one — and the direction of the difference is informative.

Why this matters

The sentence you wrote in Chapter 1 was a belief — a single claim you disagreed with, stated in prose. The document you just wrote is a thesis — a structured argument with named elements, defined failure conditions, and a clock. The distance between those two documents is the distance between having an opinion and having a framework.

In Chapter 8, you will build the agent fleet architecture that automates the monitoring side of this process — the ongoing comparison of thesis against reality. In Chapter 9, you will run this entire workflow end-to-end for three companies. But the core habit is what you practiced today: write it down, attack it, revise it, date it.

The document does not make you right. It makes you accountable to your past self — the version of you who made the decision with the information available at the time, before the outcome reshaped your memory of what you believed.

The thesis you never write

Most investors will read this chapter, nod, and not write a thesis. They will continue holding beliefs that mutate with every earnings report, defending positions they cannot articulate, selling when they are scared and buying when they are excited. Not because they lack intelligence. Because writing a thesis and sticking to the discipline of reviewing it requires confronting the possibility that you are wrong — repeatedly, on a schedule, with evidence.

That confrontation is the entire skill. Everything else in investing — the financial models, the statement analysis, the fleet architecture — is infrastructure that serves this one moment: you, sitting with your own thesis, comparing it honestly against what happened, and deciding what to do next.

The investors who do this are not smarter. They are more honest with themselves, more often, for longer. Over a decade, that compounds.

Chapter 8 covers the five core patterns for commanding an agent fleet: delegation, verification, iteration, composition, and failure detection. The thesis you wrote today becomes one input to the monitoring workflow you will build there.